COMMUNITY SAVINGS BANK

101 E. Union St.

Edgewood, Iowa 52042

ASSESSMENT AREA

Clayton County: All Census Tracts

Delaware County: All Census Tracts

Linn County: All Census Tracts

Dubuque County: Census Tracts 0102.01, 0102.02, 0104.00, and 0105.00

(March 2023 kjb)

OFFICE CLOSINGS AND OPENINGS DURING THE PAST TWO YEARS

Garnavillo Branch Relocated from 101 South Main Street Garnavillo Iowa 52049 to 103 West Clayton Street Garnavillo Iowa 52049

(April 2024 kjb)

LOAN TO DEPOSIT RATIO

March 31, 2023 – 92%

June 30, 2023 – 88%

September 30, 2023 – 84%

December 31, 2023 – 88%

(April 2024 kjb)

HOME MORTGAGE DISCLOSURE ACT NOTICE

The HMDA data about our residential mortgage lending are available online for review. The data shows geographic distribution of loans and applications; ethnicity, race, sex, age, and income of applicants and borrowers; and information about loan approvals and denials. HMDA data for many other financial institutions are also available online. For more information, visit the Consumer Financial Protection Bureau’s Website (www.consumerfinance.gov/hmda).

(March 2023 kjb)

COMMUNITY SAVINGS BANK BRANCHES

Cedar Rapids* Monday thru Friday

3414 Mount Vernon Road SE 9:00 AM – 5:00 PM

Cedar Rapids, Iowa 52403

Phone: 319-363-0577

Fax: 319-363-0578

MSA 16300, Census Tract .00016

Coggon* Monday thru Thursday/Lobby Friday/Lobby

203 East Main Street 9:00 AM – 4:00 PM 9:00 AM – 5:00PM

PO Box 139

Coggon, Iowa 52218 Monday thru Thursday/Drive-Up Friday/Drive-Up

Phone: 319-435-2551

Fax: 319-435-2555 8:30 AM – 4:00PM 8:30 AM – 5:00 PM

MSA 16300, Census Tract 0101.00

Dyersville* Monday thru Thursday Friday

1211 12th Avenue SE 8:30 AM – 4:00 PM 8:30 AM – 5:00PM

Suite 103

Dyersville, Iowa 52040

Phone: 563-875-6296

Fax: 563-875-6272

MSA 20220, Census Tract 0105.00

Earlville* Monday thru Thursday Friday Saturday (Drive-Thru Only)

106 Northern Avenue 9:00 AM – 3:00 PM 9:00 AM – 4:00 PM 8:30 AM – 11:00 AM

Earlville, Iowa 52041

Phone: 563-923-3145

Fax: 563-923-4945

MSA NA (outside of MSA), Census Tract 9501.00

Edgewood* Monday thru Friday Saturday (Drive-Thru Only)

101 East Union Street 9:00 AM – 3:00 PM 8:30 AM – 11:00 AM

Edgewood, Iowa 52042

Phone: 563-928-6425

Fax: 563-928-6240

MSA NA (outside of MSA), Census Tract 9502.00

Garnavillo* Monday thru Thursday Friday

103 West Clayton Street 8:30 AM – 4:00 PM 8:30 AM – 5:00PM

Garnavillo, Iowa 52049

Phone: 800-828-2318

Fax: 563-964-2485

MSA NA (outside of MSA), Census Tract 0701.00

Guttenberg* Monday thru Friday

502 South Highway 52 8:30 AM – 4:00 PM

Guttenberg, Iowa 52052

Phone: 563-252-1048

MSA NA (outside of MSA), Census Tract 0704.00

Manchester* Monday thru Thursday Friday Saturday (Drive-Thru Only)

221 East Main Street 9:00 AM – 4:00 PM 9:00 AM – 5:00 PM 8:30 AM – 11:00 AM

Manchester, Iowa 52057

Phone: 563-927-4014

Fax: 563-927-2411

MSA NA (outside of MSA), Census Tract 9503.00

Marion* Monday thru Friday Saturday

1295 Blairs Ferry Road 9:00 AM – 5:00 PM Not Open

Marion, Iowa 52302

Phone: 319-447-2551

Fax: 319-447-2556

MSA 16300, Census Tract 0003.00

Robins* Monday thru Friday Saturday (Drive-Thru Only)

101 Robins Square Court 9:00 AM – 5:00 PM 8:30 AM – 11:00 AM

Robins, Iowa 52328

Phone: 319-294-2783

Fax: 319-294-2784

MSA 16300, Census Tract 0002.06

*24 Hour ATM Available

COMMUNITY SAVINGS BANK SERVICE CHARGE MENU

Account activity printout (current month) * $1.87

Account balancing assistance ($10.00 min.) per hour * $18.69

Account Closed within 90 days * $14.01

(Charge not applicable to the following checking account types:

Simply Free Checking, Classic 50 Checking, VIP Direct Checking,

Ultimate Interest Checking, Simply Free Business Checking,

Business Interest Checking and Commercial Checking.)

Account Research ($10.00 min.)/per hour $18.69

Bank Sweep Manager $28.00

Cashier’s Check – (non CSB Bankclub Member) $5.00

Check Cashing non-customer ($5.00 min.) 3% of amount

Coin Counting non-customers ($5.00 min.) 5% of amount

Copy of extra statement * (per month) $2.80

Counter Checks $1.00 per 5 checks

CSB Debit Card- Annual Fee * (2 card limit) $12.00

CSB Debit Card Replacement * (per card) $18.69

CSB Debit Card Chargeback Research * (per hour) $18.69

CSB Debit Card Hotcard * (includes re-issuance fee) $18.69

Deposit Book (duplicate pad) $9.35

Fax (per page) $2.00

Foreign/Canadian deposited items * $23.37

Garnishments/Levies $50.00

Gift Card $4.95

Inactive Account Fee $10.00

Medallion Signature $10.00 (CSB Customer)

$50.00 (non-CSB Customer)

Mortgage amortization schedule $10.00

Night Deposit Key Deposit/Lost $25.00

Night Deposit Bag (Locking) $25.00

Night Deposit Bag (Zipper) $5.00

Notary (Non-customer) $2.00

Outgoing ACH Recurring (per item) $5.00

Overdraft – per item (Consumer limit of 5 per day) *** $30.00

Paper Statements (per month) $2.80

Personal Money Order (under $5000.00)– (non CSB Bankclub Member) $3.00

Photocopy (Black/White) $.25

Photocopy (Color) $.50

Pre-Authorized Automatic Transfer to avoid Overdraft Charge* $4.67

Return Item (NSF) (per presentment) $30.00

Safe Deposit (Replacement key) $15.00

Select Line of Credit- Annual Fee $40.00

Special Statement cut-off* $4.67

Special Statement handling (waived if E-statement) * $4.67

Stop Payment* $28.04

Travel Card Purchase Card $9.95

Travel Card Reload Card $4.95

Wire Transfer Incoming $10.00

Wire Transfer Domestic outgoing $25.00

Wire Transfer International Outgoing $50.00

Undeliverable Mail Fee $3.00

Personalized Checks, cost will vary.

*Applicable service charges are subject to Iowa State tax, Local Option tax, and Iowa School Local Option Tax

***Overdrafts can be created by check, in-person withdrawal, ATM withdrawal, or other electronic means.

(March 2024 kjb)

COMMUNITY SAVINGS BANK MORTGAGE LOAN PROGRAMS

The following mortgage loan programs are offered by Community Savings Bank:

- Conventional Uninsured (Less than 80% LTV Loans)

- Conventional Insured (Loans with LTV’s of greater than 80% insured by Private Mortgage Insurance)

- In-house Mortgages (For borrowers that may not meet secondary market investor guidelines at the current time)

- IFA FirstHome & IFA FirstHome Plus and Homes for Iowans and Homes for Iowans Plus (Offered through Iowa Finance Authority IFA) Offers low or no down payment fixed rate programs to qualified borrowers.

- IFA Grants are available in conjunction with IFA FirstHome Plus and IFA Homes for Iowans Plus programs for qualified borrowers. We work with IBMC (Iowa Bankers Mortgage Corporation) for the grant programs.

- FHLB HomeStart Grant-Funds are available for $7,500 Down Payment Assistance Grants to qualified low-income first-time homeowner households.

- Mortgage Credit Certificates (MCC’s) Allows the borrower to receive a Federal Tax Credit for a percentage of the interest paid on their home loan. This is funded from year to year by the Iowa Legislature.

- MHOA Military Home Ownership Assistance Grants administered by the Iowa Finance Authority.

- USDA Rural Development Guarantee Loans Zero percent down 30-year mortgage with a RD Guarantee instead of PMI

- Agri-Access Rural Living Loan This program is for rural homes that appraisals may not meet the standard secondary market criteria due to number of acres. We work with IBMC for this program.

- HOAP Program (forgivable grant for improvements—offered through cities)

- Community Seconds Program for cities that are offering incentive to build or rehab in certain parts of the city.

- OSWAP (Onsite Wastewater Assistance Program) Low-interest loans for on-site septic system replacement.

We are able to offer most loan programs offered through the following secondary market investors: Conforming, non-conforming loans and government loans.

Fannie Mae, Universal Lending, AgriAccess, Iowa Finance Authority and Iowa Bankers Mortgage Corporation.

Additionally, we are always looking for new investors, and new programs, that will help a wider variety of borrowers with their mortgage financing needs. This would include low-income borrowers, borrowers with better incomes but no/low down payment, borrowers seeking jumbo financing, and everyone in-between.

(March 2023 kjb)

COMMUNITY SAVINGS BANK SERVICES PROVIDED

Checking Accounts Savings Accounts Wealth Management

Individual Retirement Accounts Private Business Account Manager Money Orders

Cashier’s Checks Stop Payment Orders Wire Transfer Service

Overdraft Protection Corporate Sweep Manager Private Education Loans

Gov’t Guaranteed Student Loan Access Direct Deposit ACH Origination

Safe Deposit Box Night Deposit Box SHAZAM Debit Cards

Escrow Service Notary Service Tax Collection Service

Purchase & Sales of Securities Fax Service Mobile Banking

US Savings Bonds through TreasuryDirect.Gov Mobile Deposit

Internet Online Banking & Bill Pay Mobile Website Telephone Money Line Banking

Merchant Remote Capture Direct Business Loans Website Savings Account Applications

Website Consumer Loan Application Gift Cards Website Mortgage Loan Applications

Credit Cards through Elan Direct Consumer Loans Direct Agricultural Loans

Website Business Loan Applications Residential Mortgage Loans HELOC

Merchant Card Processing

**We are an Equal Housing Lender and Member FDIC

(March 2023 kjb)

COMMUNITY SAVINGS BANK DEPOSIT PRODUCTS

Personal Checking

Smart Checking

- Available to customers ages 18 or under

- Quarterly Educational Newsletter

- Secure Parental Oversight

- Teen-owned Debit Card

- Free Community Savings Bank standard checks

- No monthly maintenance fee

- No minimum balance requirements

- Unlimited check writing

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Person-to-person (P2P) payments available

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Nationwide surcharge-free ATM access via the SHAZAM Privileged Status ATM network

- $50 minimum deposit to open

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Simple Checking

- Simple checking account

- Free Community Savings Bank standard checks

- No monthly maintenance fee

- No minimum balance requirements

- Unlimited check writing

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Person-to-person (P2P) payments available

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Nationwide surcharge-free ATM access via the SHAZAM Privileged Status ATM network

- $50 minimum deposit to open

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

VIP Direct Checking

- Competitive interest on entire balance

- Free Community Savings Bank standard checks

- No monthly maintenance fee

- No minimum balance requirements

- Unlimited check writing

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free CSB Debit Card

- Nationwide surcharge-free ATM access via the SHAZAM Privileged Status ATM network

- $50 minimum deposit to open

*Interest accrues daily based on daily available balance paid monthly.

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Ultimate Interest Checking

- Higher interest rate with a balance of $1,000 and above

- Free Community Savings Bank standard checks

- Avoid the $6 monthly maintenance fee by maintaining a $1,000 minimum daily balance

- Unlimited check writing

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free CSB Debit Card

- Nationwide surcharge-free ATM accessvia the SHAZAM Privileged Status ATM network

- $50 minimum deposit to open

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Personal Savings

Regular Savings Account

- Straightforward savings account

- Avoid the $3.33 monthly maintenance fee by maintaining a $100 minimum daily balance

- 6 free withdrawals per month; $1 fee for withdrawals in excess thereafter

- Free online banking

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- $50 minimum deposit to open

Star Plus Money Market Account

- Competitive, tiered interest

- Higher balances earn higher rates

- Interest accrued daily and paid monthly

- Enjoy flexibility with enhanced access to funds, including direct check writing:

- Unlimited in-person withdrawals or by mail

- 6 free transactions per month by pre-authorized automatic, telephone, checks, drafts, or other similar order; $5 per transaction in excess thereafter

- Avoid the $10.00 monthly maintenance fee by maintaining a $2,500 minimum daily balance

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Person-to-person (P2P) paymentsavailable

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Nationwide surcharge-free ATM accessvia the SHAZAM Privileged Status ATM network

- $2,500 minimum deposit to open

Christmas Club Account

- Set aside little by little, year-round for holiday expenses

- Competitive interest on entire balance

- No monthly maintenance fee

- No minimum balance requirements

- Make deposits at any time, in any amount you feel comfortable with

- Avoid holiday-induced debt and stress

- Funds automatically deposited to a Community Savings Bank account in November*

- Early withdrawal will result in a penalty*

- Free online banking

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- $1 minimum deposit to open

*All interest earned will be credited annually. You will forfeit all accrued interest if the account is closed prior to it being credited to your account. Minimum deposit to open the account is $1.00.

Vacation Club Account

- Set aside little by little, year-round for vacation expenses

- Competitive interest on entire balance

- No monthly maintenance fee

- No minimum balance requirements

- Make deposits at any time, in any amount you feel comfortable with

- Rest easy right from the start; avoid unnecessary debt

- Funds automatically deposited to a Community Savings Bank account in May*

- Early withdrawal will result in a penalty*

- Free online banking

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- $1 minimum deposit to open

*All interest earned will be credited annually. You will forfeit all accrued interest if the account is closed prior to it being credited to your account. Minimum deposit to open the account is $1.00.

Youth Savings Account

- Available to young savers up to 12 years old

- Competitive interest on entire balance

- No monthly maintenance fee

- No minimum balance requirements

- Establishes the importance and know-how of saving money from an early age

- 6 free transactions per month by pre-authorized automatic, telephone, checks, drafts, or other similar order; $1 per transaction in excess thereafter

- Free online banking

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- $50 minimum deposit to open

Health Savings Account (HSA)

- Greater personal control over healthcare management and expenses

- Prepare for qualified medical expenses

- Earn interest above standard savings on entire balance

- Receive higher rates on larger deposits

- An HSA provides triple tax savings:

- Tax deductions when you contribute to your account

- Tax-free earnings through investment

- Tax-free withdrawals for qualified medical, dental, vision expenses, and more*

- Contributions are tax-free and can be made by you, your employer, or a third party

- Funds can be withdrawn at any time**

- No monthly maintenance fee

- No minimum balance requirements

- Unused funds remain in account year after year; no "use it or lose it" policy

- Keep your HSA in your name, regardless of career or life changes

- Federally insured by FDIC

- $50 minimum deposit to open

Eligibility

Most adults under 65 who are not enrolled in Medicare and are covered under a high-deductible health plan (HDHP) can qualify for an HSA, but it is up to the account holders to determine their own eligibility. Please contact your tax advisor for further eligibility requirements.

*Consult a tax advisor.

**You can withdraw funds at any time for any purpose. However, if funds are withdrawn for reasons other than qualified medical expenses, the amount withdrawn will be included as taxable income, and is subject to a 10% penalty.

First-Time Homebuyer Savings Accounts

The State of Iowa has established an Iowa First-Time Homebuyer Savings Account program, which may offer tax advantages on savings for qualified home purchases in Iowa. Accounts may be established by qualifying first-time homebuyers or by others on behalf of qualifying first-time homebuyers. It is important to understand the requirements of the program and you may want to consult your tax advisor.

Learn More About First-Time Homebuyers Savings Account

Home Buyer Savings Includes:

- No minimum to open.

- Earn variable interest rates.

- May claim a deduction for Iowa individual income.

You can learn more about this program by visiting https://tax.iowa.gov/ and searching First-Time Homebuyer Savings Account.

Certificates of Deposit (CDs)

- Fixed rates, higher than regular savings

- Receive higher rates by selecting a longer term

- Provides more guarantee than other risky investments

- Set aside for future savings goals

- A wide range of terms available (from 90 days to 5 years)

- No setup or maintenance fees

- Early withdrawals subject to penalty*

- $1,000 minimum deposit to open

*Early withdrawals may result in penalties. Penalties vary depending on the CD.

Individual Retirement Accounts (IRAs)

- Competitive interest above standard savings rates

- Traditional and Roth IRA options

- No setup fees

- No monthly or annual maintenance fees

- $5,500 contribution limit per year

- Additional $1,000 "catch-up" contribution allowed for ages 50+

- Funds can be used to purchase CDs within IRA

- No minimum deposit to open

Traditional & Roth IRAs

Traditional IRA

- No income limits to open

- No minimum contribution requirement

- Contributions are tax deductible on state and federal income tax*

- Earnings are tax deferred until withdrawal (when usually in lower tax bracket)

- Withdrawals can begin at age 59½

- Early withdrawals subject to penalty**

- Mandatory withdrawals at age 70½

Roth IRA

- Income limits to be eligible to open Roth IRA***

- Contributions are NOT tax deductible

- Earnings are 100% tax free at withdrawal*

- Principal contributions can be withdrawn without penalty*

- Withdrawals on interest can begin at age 59½

- Early withdrawals on interest subject to penalty**

- No mandatory distribution age

- No age limit on making contributions as long as you have earned income

*Subject to some minimal conditions. Consult a tax advisor.

**Certain exceptions apply, such as healthcare, purchasing first home, etc.

***Consult a tax advisor.

COVERDELL ESA

College isn’t getting any cheaper. That makes saving for your child’s education so important. Our Coverdell Education Savings Account (ESA) provides a safe, tax-free place to set funds aside — and earn competitive interest.

- Set aside funds for your child's education

- No setup or annual fee

- Dividends grow tax-free

- Withdrawals are tax-free and penalty-free when used for qualified education expenses*

- Designated beneficiary must be under 18 when contributions are made

- To contribute to an ESA, certain income limits apply**

- Contributions are not tax deductible

- $2,000 maximum annual contribution per child

- The money must be withdrawn by the time he or she turns 30***

- The ESA may be transferred without penalty to another member of the family

- $250 minimum deposit to open

*Qualified expenses include tuition and fees, books, supplies, board, etc.

**Consult your tax advisor to determine your contribution limit.

***Those earnings are subject to income tax and a 10% penalty.

Business Checking Accounts

Simple Business Checking

- Simplified checking solution

- No monthly maintenance fee

- No minimum balance requirements

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Business servicesavailable

- $50 minimum deposit to open

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Business Interest Checking

- Available to non-profit organizations and sole proprietorships

- Competitive tiered interest on entire balance

- Avoid the $6 monthly maintenance fee by maintaining a $1,000 minimum daily balance

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Business servicesavailable

- $50 minimum deposit to open

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Commercial Checking

- Ideal for businesses with large transaction volumes

- Unlimited monthly transactions available at low per-item fees

- $10 monthly maintenance fee

- Receive an earnings credit to offset or minimize monthly fees incurred***

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- Business services available

- $50 minimum deposit to open

***Earnings credit based on balance requirements.

*Other fees such as overdraft, return (NSF), paper statements, etc. may apply. See fee schedule for details. Offer good on personal accounts only. Ask us about our great business checking plans including Simple Business Checking. Bank rules and regulations apply. Minimum opening deposit is only $50. Ask us for details.

Business Savings Accounts

Regular Business Savings Account

- Convenient savings solution

- Competitive interest on balances of $100 or more

- Avoid the $3.33 monthly service fee by maintaining a $100 minimum daily balance

- 6 free withdrawals per month; $1 fee for withdrawals in excess thereafter

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- $100 minimum deposit to open

Business Star Plus Money Market Account

- Competitive, tiered interest

- Higher balances earn higher rates

- Interest accrued daily and paid monthly

- Enjoy flexibility with enhanced access to funds, including direct check writing:

- Unlimited in-person withdrawals or by mail

- 6 free transactions per month by pre-authorized automatic, telephone, checks, drafts, debit cards, or other

- similar order; $5 per transaction in excess thereafter

- Avoid the $10.00 monthly service fee by maintaining a $2,500 minimum daily balance

- Free online banking & bill pay

- Free mobile banking with mobile deposit

- Free e-statements

- Free telephone banking

- Free Mastercard® debit card

- $2,500 minimum deposit to open

Business Retirement Accounts

Simplified Employee Pension (SEP IRA)

- Ideal for businesses of any size or self-employed individuals

- Gain the respect of your employees

- Help employees reach their retirement savings goals

- Employee always has complete ownership of all SEP IRA money

- Earn competitive interest on entire balance

- Contributions are tax deductible; your business pays no taxes on earnings

- Contributions made only by the employer

- Only self-employed may make contributions on their own behalf

- Little to no documents to file with government

- Inexpensive to set up and operate

- Flexible annual contributions – good plan if cash flow is unpredictable

- Can contribute up to 25% of each participant's annual compensation (earned income)

- Or, up to the maximum allowable limit for current plan year, whichever is less

- Must contribute equally for all employees

- Employee must first establish a traditional IRA, in which the employer will deposit SEP contributions

- No minimum deposit to open

Savings Incentive Match Plan for Employees (SIMPLE IRA)

- Available to any small business – generally with 100 or fewer employees

- Gain the respect of your employees

- Employees have the option to make self-contributions

- Help employees reach their retirement savings goals

- Employee always has complete ownership of all SIMPLE IRA money

- Earns a competitive interest rate

- Employer must not have any other retirement plan

- Minimal paperwork necessary; no filing requirements

- Inexpensive to set up and operate

- Lower contribution limits than some other retirement options

- Employees share responsibility of growing their retirement

- Each year, employer is required to contribute:

- Matching contribution up to 3% of compensation, or

- 2% non-elective contribution for each eligible employee

- No minimum deposit to open

COMMUNITY SAVINGS BANK LOAN PRODUCTS

Personal Loans

Student Loans

We work with ISL Education Lending to offer private loans to help you pay for college as well as refinance existing student loans. ISL Education Lending is a nonprofit organization with decades of student loan experience offering lower-priced loans.*

ISL Education Lending offers:

- Loans for college students.

- A loan option for parents and family members who wish to borrow on behalf of a college student.

- Multiple student loan refinance options.

In addition, they offer multiple scholarship opportunities and free college planning tools to help students and families avoid overborrowing and plan smart for life during and after college.

Home Mortgage Loans

- Competitive rates for home purchase, refinance, or construction

- Several financing programs available

- Loan advisors with working knowledge of the local real estate market

Home Equity Loans

- Competitive rates for short-term or ongoing needs

- The existing equity in your home is used as collateral

- Term loan and line of credit options available

Parent Refinance Loan

Student Loan Consolidation

- Competitive rates to consolidate and refinance one or multiple loans

- One easy payment to manage

- Private and Federal loans are eligible for consolidation

Auto Loans

- Competitive rates on new or used vehicles*

- A wide range of terms customized to your unique situation

- Pre-approval available for extra bargaining power

Personal Term Loans

- Competitive rates for a wide variety of personal needs

- Repayment terms customized to fit your unique needs

- Local decision-making and processing

Business Loans

Small Business Administration (SBA) Loans

- Government-assisted financing for qualifying businesses

- A wide range of lending options available

- Generally lower down payments and extended terms

Business Term Loans

- Competitive rates for a wide range of business expenses

- Repayment terms customized to your business needs

- Local decision-making and processing

Business Lines of Credit

- Competitive rates for long-term or seasonal business needs

- Funds available right as you need them

- Only pay interest on the part that's used

Accounts Receivables Financing

- Unlocks working capital and enhances cash flow

- Provides quick access to cash when you need it

- More flexibility than traditional financing

Commercial Real Estate Loans

- Competitive rates to build, buy or refinance commercial properties

- Available for owner-occupied or investment properties

- Loan advisors with working knowledge of the local real estate market

Agricultural Loans

Equipment Loans

- Competitive rates for new or used equipment

- Meet needs without cutting into working capital or savings

- Avoid lapsed periods in production and outdated equipment

Agriculture Real Estate Loans

- Competitive rates to buy or refinance agriculture properties

- Repayment terms customized to fit your operation's needs

- Loan advisors with working knowledge of the local real estate market

Operating Lines of Credit

- Competitive rates for long-term or seasonal agriculture needs

- Funds available right as you need them

- Only pay interest on the part that's used

(March 2023 kjb)

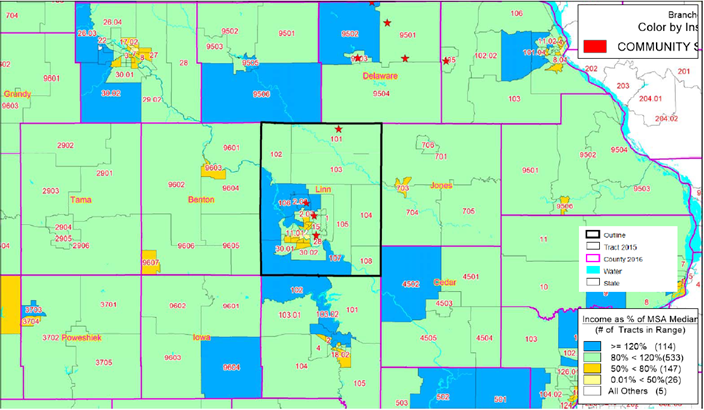

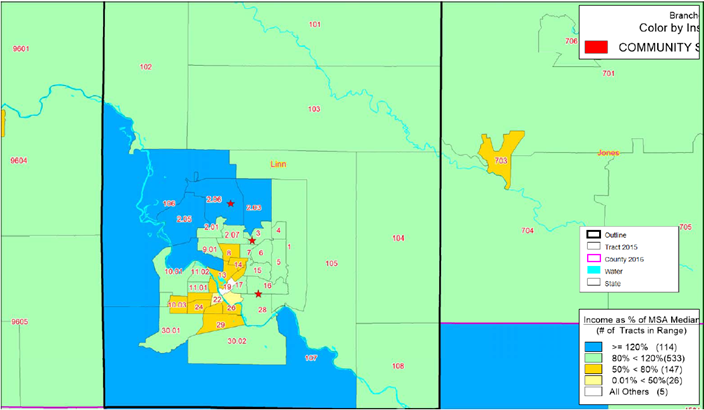

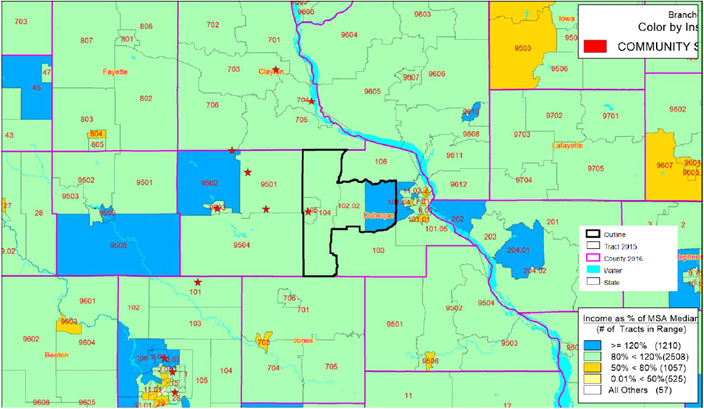

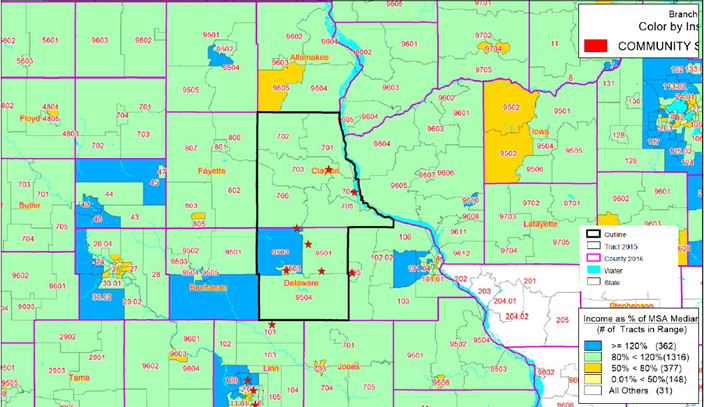

COMMUNITY SAVINGS BANK ASSESSMENT AREA MAP 2021

Community Savings Bank Cert 14633

Edgewood, Iowa

ACS - Cedar Rapids Metro AA - Incomes

Community Savings Bank Cert 14633

Edgewood, Iowa

ACS - Cedar Rapids Metro AA - Income CLOSER

Community Savings Bank Cert 14633

Edgewood, Iowa

ACS - Dubuque Metro AA - Income

Community Savings Bank Cert 14633

Edgewood, Iowa

ACS - Non-Metro AA - Income

PUBLIC DISCLOSURE

May 24, 2021

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

Community Savings Bank Certificate Number: 14633

101 East Union Street Edgewood, Iowa 52042

Federal Deposit Insurance Corporation Division of Depositor and Consumer Protection Kansas City Regional Office

1100 Walnut Street, Suite 2100 Kansas City, Missouri 64106

This document is an evaluation of this institution’s record of meeting the credit needs of its entire community, including low- and moderate-income neighborhoods, consistent with safe and sound operation of the institution. This evaluation is not, nor should it be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion, or opinion of the federal financial supervisory agency concerning the safety and soundness of this financial institution.

TABLE OF CONTENTS

INSTITUTION RATING........................................................................................................ 1

DESCRIPTION OF INSTITUTION........................................................................................................ 2

DESCRIPTION OF ASSESSMENT AREAS........................................................................................................ 3

SCOPE OF EVALUATION........................................................................................................ 3

CONCLUSIONS ON PERFORMANCE CRITERIA....................................................................................................... 5

DISCRIMINATORY OR OTHER ILLEGAL CREDIT PRACTICES REVIEW..................................................................................................... 11

NON-METRO ASSESSMENT AREA – Full-Scope Review...................................................................................................... 12

CEDAR RAPIDS METRO ASSESSMENT AREA – Full-Scope Review..................................................................................................... 17

DUBUQUE METRO ASSESSMENT AREA – Full-Scope Review..................................................................................................... 24

APPENDICES...................................................................................................... 29

INTERMEDIATE SMALL BANK PERFORMANCE CRITERIA.................................................................................................. 29

GLOSSARY.................................................................................................. 30

INSTITUTION RATING

INSTITUTION’S CRA RATING: This institution is rated Satisfactory.

An institution in this group has a satisfactory record of helping to meet the credit needs of its assessment area, including low- and moderate-income neighborhoods, in a manner consistent with its resources and capabilities.

Community Savings Bank (CSB)’s satisfactory Community Reinvestment Act (CRA) performance under the Lending Test and Community Development Test supports the rating. The following points summarize the bank’s Lending Test and Community Development Test performance.

The Lending Test is rated Satisfactory.

- The loan-to-deposit ratio is reasonable given the institution’s size, financial condition, and credit needs of the assessment areas.

- A majority of small farm, small business, and home mortgage loans are inside the bank’s assessment

- The geographic distribution of loans reflects reasonable dispersion throughout the assessment area

- The distribution of borrowers reflects reasonable penetration among farms and businesses of different revenue sizes, as well as individuals of varying income

- The institution did not receive any CRA-related complaints since the previous evaluation; therefore, this factor did not affect the rating.

The Community Development Test is rated Satisfactory.

- Overall, the institution demonstrated adequate responsiveness to the community development needs of its assessment areas through community development loans, qualified investments, and the provision of community development services. Examiners considered the institution’s capacity, as well as the need and availability of opportunities in the assessment areas.

DESCRIPTION OF INSTITUTION

CSB is a commercial bank headquartered in Edgewood, Iowa, which is located in eastern Iowa. CSB is wholly-owned by Community Financial Corporation of Edgewood, Iowa. CSB received a Satisfactory rating at its previous FDIC Performance Evaluation, dated May 15, 2018, which was performed using Interagency Intermediate Small Institution Examination Procedures. CSB currently operates from 10 full-service offices distributed amongst three assessment areas in eastern Iowa. The institution closed a branch office in Greeley, Iowa on February 14, 2020, but there was no impact to the bank’s assessment areas.

CSB offers various loan products including agricultural, commercial, home mortgage, and consumer loans. CSB’s primary focus is on agricultural lending, with a secondary focus on commercial lending. The bank also offers financing alternatives through the following loan programs: Small Business Administration (SBA), United States Department of Agriculture (USDA) Rural Development, Farm Service Agency, Federal Housing Administration, Veterans Administration, Federal Home Loan Bank Homeownership grants, and Iowa Finance Authority.

These programs are generally designed to assist small businesses, small farmers, veterans, and low- or moderate-income individuals who may not qualify for loans through conventional financing methods. Secondary market financing options are available for qualifying borrowers. The bank also participated in the SBA’s Paycheck Protection Program (PPP) during the review period. This program provided financial aid to businesses impacted by closings resulting from the COVID-19 pandemic.

The institution provides a variety of deposit products including checking, savings, and certificates of deposit. CSB participates in the Certificate of Deposit Account Registry Services program, and offers trust and wealth management services. Alternative banking services include internet banking, bill pay services, telephone banking, mobile banking, mobile deposit, and night deposit facilities. CSB also operates deposit-taking ATMs located at all 10 bank locations, as well as interactive teller machines at the Mount Vernon Road, Guttenberg, and Manchester branch locations.

Assets totaled approximately $501.0 million as of March 31, 2021, representing an increase of 16.3 percent since the March 31, 2017, Consolidated Reports of Condition and Income (Call Report).

Total deposits equaled approximately $405.4 million, representing a 15.8 percent increase, and total loans were approximately $344.5 million, representing an increase of 6.5 percent during the same timeframe. Portfolio concentrations have remained generally consistent, though commercial lending has increased approximately 10.3 percent over the period reviewed. Management attributed the growth in loans and deposits to stimulus and PPP activity, as well as organic growth occurring as a result of normal operations. Though commercial lending activity in the portfolio has surpassed agricultural lending overall, management again attributed the increase to the influx of temporary PPP loan activity and stated that the institution’s lending focus is still primarily agricultural in nature. The composition of the loan portfolio is illustrated in the following table.

|

Loan Portfolio Distribution as of 3/31/2020 |

||

|

Loan Category |

$(000s) |

% |

|

Construction, Land Development, and Other Land Loans |

9,974 |

2.9 |

|

Secured by Farmland |

76,815 |

22.3 |

|

Secured by 1-4 Family Residential Properties |

37,574 |

10.9 |

|

Secured by Multifamily (5 or more) Residential Properties |

7,812 |

2.3 |

|

Secured by Nonfarm Nonresidential Properties |

86,509 |

25.1 |

|

Total Real Estate Loans |

218,684 |

63.5 |

|

Commercial and Industrial Loans |

66,142 |

19.2 |

|

Agricultural Production and Other Loans to Farmers |

43,316 |

12.6 |

|

Consumer Loans |

9,751 |

2.8 |

|

Obligations of State and Political Subdivisions in the U.S. |

1,469 |

0.4 |

|

Other Loans |

5,114 |

1.5 |

|

Lease Financing Receivable (net of unearned income) |

0 |

0.0 |

|

Less: Unearned Income |

0 |

0.0 |

|

Total Loans |

344,476 |

100.0 |

|

Source: Call Report |

||

Examiners did not identify any financial, legal, or other impediments that affect the bank’s ability to meet the credit or community development needs of its assessment areas.

DESCRIPTION OF ASSESSMENT AREAS

The CRA requires each financial institution to define one or more assessment areas within which its CRA performance will be evaluated. CSB has defined three assessment areas within the state of Iowa, and the rating stated in this performance evaluation is an overall rating of the institution’s performance in those assessment areas. Refer to the discussion regarding each individual assessment area for detailed information.

SCOPE OF EVALUATION

General Information

This evaluation covers the period from the prior evaluation dated May 15, 2018, to the current evaluation date of May 24, 2021. Examiners used the Interagency Intermediate Small Institution Examination Procedures to evaluate CSB’s CRA performance. These procedures include the Lending and Community Development Tests, which are described in detail in the Appendix.

Examiners conducted full-scope reviews of the institution’s assessment areas to evaluate performance. As shown in the following table, the vast majority of CSB’s loans, deposits, and branches are in the Non-Metro Assessment Area. Therefore, the institution’s performance in the Non-Metro Assessment Area received the most weight in the overall evaluation. The following table reflects the distribution of reported loans, deposits, and office locations in each assessment area.

|

Assessment Area Breakdown of Loans, Deposits, and Branches |

||||||||

|

Assessment Area |

Loans |

Deposits |

Branches |

|||||

|

# |

% |

$(000s) |

% |

$(000s) |

% |

# |

% |

|

|

Non-Metro |

3,520 |

63.7 |

217,337 |

63.8 |

268,942 |

69.7 |

5 |

50 |

|

Cedar Rapids Metro |

1,190 |

21.5 |

90,914 |

26.7 |

103,419 |

26.8 |

4 |

40 |

|

Dubuque Metro |

817 |

14.8 |

32,622 |

9.5 |

13,688 |

3.5 |

1 |

10 |

|

Total |

5,527 |

100.0 |

340,873 |

100.0 |

386,049 |

100.0 |

1 |

100.0 |

|

Source: Bank Records as of 5/4/2021; FDIC Summary of Deposits (6/30/2020) |

||||||||

Activities Reviewed

Examiners determined that the institution’s major product lines are agricultural, commercial, and residential real estate loans. This conclusion was based on the institution’s business strategy, loan portfolio distribution, and institution records regarding the number and dollar volume of loans originated or renewed during the evaluation period. Therefore, examiners reviewed small farm, small business, and home mortgage lending for this evaluation. Overall, small farm lending received the greatest weight in the Non-Metro and Dubuque Metro assessment areas due to management’s stated business focus on agricultural lending in those locations. Small farm lending was not reviewed in the Cedar Rapids Metro Assessment Area, given management’s stated business focus of commercial lending in that assessment area and very limited activity during the review period.

For the Assessment Area Concentration review, examiners evaluated lending performance based on all small farm and small business loans originated or renewed in calendar year 2020, which management indicated was indicative of lending over the entire evaluation period, as well as home mortgage loan data collected under the Home Mortgage Disclosure Act (HMDA) for 2018, 2019, and 2020. For the Geographic Distribution review, examiners evaluated lending performance based on all small business loans originated or renewed inside the Cedar Rapids Metro Assessment Area in calendar year 2020, as well as home mortgage loan data originated or purchased inside the assessment area in 2018, 2019, and 2020. The Geographic Distribution criterion was not evaluated for the Non-Metropolitan or Dubuque Metro assessment areas because there are no low- or moderate-income geographies in those areas; therefore, an analysis would not yield meaningful results. Examiners evaluated Borrower Profile performance for small farm and small business lending using a sample of loans originated inside the reviewed assessment areas in 2020 for applicable loan products. However, due to limited lending activity in the Dubuque Metro Assessment Area, examiners reviewed the entire universe of small farm and small business loans originated inside the assessment area. The Borrower Profile analysis included all home mortgage loans, within each assessment area. Details are discussed in the applicable assessment area sections. The following table provides universe and sample information.

|

Loan Products Reviewed |

||||

|

Loan Category |

Universe |

Sampled |

||

|

# |

$(000s) |

# |

$(000s) |

|

|

Small Farm* |

312 |

34,772 |

79 |

10,553 |

|

Small Business* |

337 |

38,872 |

92 |

10,398 |

|

HMDA 2018 |

263 |

26,611 |

|

|

|

HMDA 2019 |

294 |

34,957 |

|

|

|

HMDA 2020 |

726 |

113,025 |

|

|

|

Source: * 2020 Bank Data; 2018-2020 HMDA Reported Data |

||||

For small farm and small business conclusions, 2020 D&B data provided a standard of comparison. When arriving at home mortgage conclusions, 2015 ACS Census data and HMDA aggregate lending data provided a standard of comparison. Examiners primarily focused on CSB’s lending performance in comparison to HMDA aggregate data, when available, as this is typically a better indicator of market conditions and loan demand in the assessment areas. Regarding lending performance for home mortgage, this evaluation presents information for 2019, the most recent year for which aggregate lending data is available. HMDA data for 2018 and 2020 was reviewed to ensure that performance was consistent with 2019. Commentary may be included relating to 2018 and 2020 data to support performance conclusions.

Examiners obtained the data necessary for this evaluation from reported loan data, other institution records, individual customer loan files, interviews with institution management, and other information gathered as part of the examination process. Examiners analyzed lending performance by both the number and dollar volume of loans; however, the performance by number of loans is emphasized, as it is generally a better indicator of the number of small farms, small businesses, and individuals served.

For the Community Development Test, examiners reviewed management-presented data on community development loans, qualified investments, and community development services provided since the prior CRA evaluation.

Effective March 1, 2020, the United States declared a national emergency concerning the COVID- 19 outbreak, which greatly influenced the economy. Unless otherwise noted, the economic impact of the pandemic on the assessment areas is unknown due to a lag in published data. The pandemic caused every state in the U.S. to be declared a disaster area in 2020. There were also other weather- related disasters declared during the review period that affected certain assessment area counties.

CONCLUSIONS ON PERFORMANCE CRITERIA

LENDING TEST

CSB demonstrated satisfactory performance under the Lending Test. The institution’s performance under the Loan-to-Deposit Ratio, Assessment Area Concentration, Geographic Distribution, and Borrower Profile criteria support this conclusion. The following is a discussion of each performance criterion and their support for the institution’s overall rating.

Loan-to-Deposit Ratio

CSB’s loan-to-deposit ratio is reasonable, given the institution’s size, financial condition, and assessment areas’ credit needs. The institution’s net loan-to-deposit ratio, calculated from Call Report data, averaged 86.2 percent over the 12 calendar quarters from June 30, 2018, to March 31, 2021. The net loan-to-deposit ratio ranged from a high of 90.4 percent as of September 30, 2018, to a low of 83.9 percent as of December 31, 2020. The ratio has been relatively steady over the period reviewed, as total deposits and net loans have generally made gains and reductions in tandem over the reported quarters, though total deposits have grown more than net loans, leading to a slight decline in the ratio, overall.

Examiners compared CSB’s average net-loan-to-deposit ratio with those of three similarly-situated institutions to evaluate CSB’s performance. Comparable institutions were selected based on similarities in lending focus, asset size, and markets served. As shown in the following table, CSB’s ratio is similar to comparable institutions.

|

Loan to Deposit Ratio Comparison |

||

|

Bank |

Total Assets as of 3/31/2021 $ (000s) |

Average Net Loan to Deposit Ratio (%) |

|

Community Savings Bank, Edgewood, Iowa |

500,980 |

86.2 |

|

BankIowa, Cedar Rapids, Iowa |

779,435 |

96.5 |

|

FreedomBank, Elkader, Iowa |

477,448 |

97.6 |

|

Citizens State Bank, Monticello, Iowa |

461,116 |

64.3 |

|

Source: Call Reports 6/30/18 through 3/31/21 |

||

The institution also has the ability to originate mortgage loans that are subsequently sold through secondary market relationships; these loans are not included in the institution’s ratio. CSB reported originating 808 loans totaling approximately $133.3 million sold on the secondary market from May 15, 2020, to December 31, 2020. While the sale of secondary market loans does not influence the average net loan-to-deposit ratio, this activity provides liquidity to originate additional home mortgage loans. Secondary market lending is responsive to the assessment areas’ credit needs by providing long-term home mortgage financing.

Assessment Area Concentration

CSB extended a majority of its small farm, small business, and home mortgage loans inside its assessment areas, by number and dollar amount, demonstrating a willingness to extend credit in the areas it serves. Please see the following table.

|

Lending Inside and Outside of the Assessment Area |

||||||||||

|

Loan Category |

Number of Loans |

|

Dollar Amount of Loans $(000s) |

|

||||||

|

Inside |

Outside |

Total |

Inside |

Outside |

Total |

|||||

|

# |

% |

# |

% |

# |

$ |

% |

$ |

% |

$(000s) |

|

|

Small Farm |

280 |

89.7 |

32 |

10.3 |

312 |

31,840 |

91.6 |

2,932 |

8.4 |

34,772 |

|

Small Business |

261 |

77.4 |

76 |

22.6 |

337 |

28,529 |

73.4 |

10,343 |

26.6 |

38,872 |

|

Home Mortgage |

|

|||||||||

|

2018 |

220 |

83.7 |

43 |

16.4 |

263 |

20,516 |

77.1 |

6,096 |

22.9 |

26,611 |

|

2019 |

255 |

86.7 |

39 |

13.3 |

294 |

28,514 |

81.6 |

6,442 |

18.4 |

34,957 |

|

2020 |

591 |

81.4 |

135 |

18.6 |

726 |

91,145 |

80.6 |

21,880 |

19.4 |

113,025 |

|

Subtotal |

1,066 |

83.1 |

217 |

16.9 |

1,283 |

140,175 |

80.3 |

34,418 |

19.7 |

174,593 |

|

Source: Bank Data Due to rounding, totals may not equal 100.0% |

||||||||||

Geographic Distribution

The geographic distribution of loans reflects reasonable dispersion throughout the assessment areas. Examiners considered the percentage, by number, of loans in low- and moderate-income census tracts located in the Cedar Rapids Metro Assessment Area. The Non-Metro and Dubuque Metro assessment areas do not include any low- or moderate-income geographies, and a review of the Geographic Distribution criterion would not result in meaningful conclusions; therefore, this criterion was not evaluated in those areas.

Borrower Profile

Overall, the distribution of borrowers reflects reasonable penetration among farms and businesses of differing revenue sizes, as well as individuals of differing income levels. The institution’s reasonable lending performance in each assessment area supports this conclusion. Examiners focused on the percentage, by number, of loans, to farms and businesses with gross annual revenues of $1 million or less, as well as low- and moderate-income home mortgage borrowers.

Response to Complaints

The institution has not received any CRA-related complaints since the previous evaluation; therefore, this criterion did not affect the Lending Test rating.

COMMUNITY DEVELOPMENT TEST

The institution’s community development performance demonstrates adequate responsiveness to community development needs of the assessment areas through community development loans, qualified investments, and the provision of community development services. CSB’s activities support community development primarily through economic development efforts that create or retain employment; the institution has also provided support for affordable housing, community services targeted to low-and moderate-income individuals, and efforts to revitalize or stabilize low- and moderate-income or underserved middle-income geographic areas. Community development

activities that benefitted the broader statewide and/or regional area were included in the analysis, as the institution adequately responded to the needs of its assessment areas.

Information from performance evaluations of three comparable intermediate small institutions conducted during the review period was used to assess CSB’s overall performance under the Community Development Test. These institutions were chosen because of similarities in asset size, business focus, and types of assessment areas served. Overall, CSB’s performance compared favorably to the performance of these institutions.

Community Development Loans

CSB originated 1,349 community development loans totaling approximately $55.9 million during the evaluation period, which represents 16.4 percent of net loans and 11.2 percent of total assets, as of March 31, 2021. These ratios have increased significantly since the previous evaluation when community development loans represented 1.5 percent of net loans and 1.1 percent of total assets. The majority of this growth is attributed to lending conducted as part of the SBA’s PPP, which was designed to help businesses keep their workforce employed during the pandemic. However, exclusive of PPP loans, the bank’s performance significantly declined, with 53 community development loans totaling approximately $1.3 million during the current review period, compared to 125 loans totaling $4.9 million at the prior evaluation.

The referenced comparable intermediate small institutions were last evaluated with PPP loans; therefore, ratios derived from data including the PPP loans were compared. CSB compared very well with the similarly-situated institutions whose community development loans ranged from 5.7 percent to 8.4 percent of net loans, and 3.4 percent to 6.7 percent of total assets. The following tables reflect the number and dollar volume of community development lending in each category by assessment area and activity year. These tables also identify lending activities in the broader statewide or regional areas that received consideration.

|

Community Development Lending by Assessment Area |

||||||||||

|

Assessment Area |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Totals |

|||||

|

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

|

|

Non-Metro |

0 |

0 |

0 |

0 |

758 |

28,236 |

1 |

20 |

759 |

28,256 |

|

Cedar Rapids Metro |

0 |

0 |

0 |

0 |

408 |

14,463 |

0 |

0 |

408 |

14,463 |

|

Dubuque Metro |

0 |

0 |

0 |

0 |

165 |

3,240 |

0 |

0 |

165 |

3,240 |

|

Total in Assessment Areas |

0 |

0 |

0 |

0 |

1,331 |

45,939 |

1 |

20 |

1332 |

45,959 |

|

Regional Activities |

1 |

91 |

0 |

0 |

11 |

9,797 |

5 |

69 |

17 |

9,957 |

|

Total |

1 |

91 |

0 |

0 |

1,342 |

55,736 |

6 |

89 |

1,349 |

55,916 |

|

Source: Bank Data |

||||||||||

|

Community Development Lending |

||||||||||

|

Activity Year |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Totals |

|||||

|

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

|

|

2018 (Partial) |

0 |

0 |

0 |

0 |

15 |

255 |

4 |

63 |

19 |

318 |

|

2019 |

1 |

91 |

0 |

0 |

21 |

722 |

2 |

26 |

24 |

839 |

|

2020 |

0 |

0 |

0 |

0 |

567 |

35,965 |

0 |

0 |

567 |

35,965 |

|

YTD 2021 |

0 |

0 |

0 |

0 |

739 |

18,794 |

0 |

0 |

739 |

18,794 |

|

Total |

1 |

91 |

0 |

0 |

1,342 |

55,736 |

6 |

89 |

1,349 |

55,916 |

|

Source: Bank Data |

||||||||||

Examples of the CSB’s community development loan activities, where the institution has shown exceptional responsiveness, are discussed in the individual assessment area sections, if applicable. If no discussion is noted, then the institution’s performance in that assessment area was not unique and was similar to community development lending observed at other institutions.

Qualified Investments

The institution made 105 qualified investments totaling approximately $8.6 million during the evaluation period, which represents 1.7 percent of total assets and 8.75 percent of total securities, as of March 31, 2021. This represents a decrease in volume from the previous evaluation, when the percentages of total assets and total securities were 2.2 and 13.2 percent, respectively. Qualified investment activity included 78 donations totaling approximately $87,000, as well as 16 investments made in a prior period that had outstanding balances of approximately $3.6 million as of this evaluation date. Comparable institutions reported qualifying investment activity that ranged from 0.9 to 1.4 percent of total assets and 5.7 to 18.6 percent of total securities. CSB compares reasonably to these institutions. Please see the following tables.

|

Community Development Qualified Investments by Assessment Area |

||||||||||

|

Assessment Area |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Totals |

|||||

|

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

|

|

Non-Metro |

0 |

0 |

0 |

0 |

6 |

1 |

68 |

2,098 |

74 |

2,099 |

|

Cedar Rapids Metro |

0 |

0 |

2 |

1 |

4 |

6 |

3 |

1 |

9 |

8 |

|

Dubuque Metro |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

Assessment Areas Subtotal |

0 |

0 |

2 |

1 |

10 |

7 |

71 |

2,099 |

83 |

2,107 |

|

Regional Activities |

0 |

0 |

0 |

0 |

0 |

0 |

22 |

6,453 |

22 |

6,453 |

|

Total |

0 |

0 |

2 |

1 |

10 |

7 |

93 |

8,552 |

105 |

8,560 |

|

Source: Bank Records |

||||||||||

|

Qualified Investments |

||||||||||

|

Activity Year |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Totals |

|||||

|

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

# |

$(000s) |

|

|

Prior Period |

0 |

0 |

0 |

0 |

0 |

0 |

16 |

3,598 |

16 |

3,598 |

|

2018 (Partial) |

0 |

0 |

0 |

0 |

0 |

0 |

4 |

975 |

4 |

975 |

|

2019 |

0 |

0 |

0 |

0 |

0 |

0 |

5 |

2,632 |

5 |

2,632 |

|

2020 |

0 |

0 |

0 |

0 |

0 |

0 |

2 |

1,268 |

2 |

1,268 |

|

2021 (YTD) |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

|

Subtotal |

0 |

0 |

0 |

0 |

0 |

0 |

27 |

8,473 |

27 |

8,473 |

|

Qualified Grants & Donations |

0 |

0 |

2 |

1 |

10 |

7 |

66 |

79 |

78 |

87 |

|

Total |

0 |

0 |

2 |

1 |

10 |

7 |

93 |

8,552 |

105 |

8,560 |

|

Source: Bank Records |

||||||||||

Examples of the CSB’s qualified investment activities, where the institution has shown exceptional responsiveness, are discussed in the individual assessment area sections, if applicable. If no discussion is noted, then the institution’s performance in that assessment area was not unique and was similar to qualifying investments observed at other institutions.

Community Development Services

The bank received consideration for a total of 70 community development services that primarily consisted of providing support to organizations that provide economic development or revitalization or stabilization efforts in the assessment areas. CSB personnel provided technical or financial expertise to these organizations in many ways, all related to the same or similar skills used in their employment with the institution. Multiple employees have dedicated their time and resources to 25 different organizations over the review period. Most employees providing qualified services did so in an officer, president, or Board member capacity. The number of services and organizations served has slightly decreased since the prior evaluation, when the institution received consideration for a total of 86 community development services serving 30 different entities.

Similarly-situated institutions provided a range of 24 to 75 community development services; CSB compares favorably to these institutions. The following tables illustrate the bank’s community development services in each category by assessment area and activity year.

|

Community Development Services by Assessment Area |

|||||

|

Assessment Area |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Total |

|

# |

# |

# |

# |

# |

|

|

Non-Metro |

5 |

5 |

16 |

34 |

60 |

|

Cedar Rapids Metro |

0 |

1 |

1 |

0 |

2 |

|

Dubuque Metro |

0 |

0 |

8 |

0 |

8 |

|

Total |

5 |

6 |

25 |

34 |

70 |

|

Source: Bank Data |

|||||

|

Community Development Services |

|||||

|

Year |

Affordable Housing |

Community Services |

Economic Development |

Revitalize or Stabilize |

Total |

|

# |

# |

# |

# |

# |

|

|

2018 (Partial) |

2 |

4 |

5 |

10 |

21 |

|

2019 |

2 |

1 |

7 |

9 |

19 |

|

2020 |

1 |

0 |

7 |

8 |

16 |

|

2021 (YTD) |

0 |

1 |

6 |

7 |

14 |

|

Total |

5 |

6 |

25 |

34 |

70 |

|

Source: Bank Data |

|||||

The bank offers various small business and personal retail credit and deposit products, including a number of no- or low-cost accounts for business and retail customers. A transactional website is maintained, through which consumers can access online banking, permitting them to check account balances, transfer funds between accounts, and pay bills. Electronic access is also available through mobile banking and electronic statements. These services are generally free of charge to bank customers, which is beneficial to low- and moderate-income individuals.

As mentioned previously, the bank participates in various lending programs that aid small businesses, small farms, and potential homeowners. CSB also implemented the following measures to accommodate customers affected by the COVID-19 pandemic. Such efforts are considered highly responsive to the needs of low- and moderate-income individuals, small businesses, and small farms affected by the pandemic:

- Loan modifications upon request

- Overdraft fees waived upon request

- Extended information and assistance to customers regarding stimulus check deposits

- Free cash advances on the debit cards that were issued for the relief checks to customers and non-customers

- Waived fees for any purchases or loads of gift cards and travel cards in April

- Developed the “Skip-a-Pay” program, allowing consumer loan customers to forgo one payment in the month of April or May 2020, upon request. There were 188 participants in the program, 52 percent of which were identified as low- or moderate-income

Retail banking services and loan programs are consistent among all of CSB’s assessment areas. Two branch offices, two ATMs, and one interactive teller machine are located in underserved middle-income geographies. Other qualitative examples of community development services where the bank has been the most responsive are discussed in the individual assessment area sections of this evaluation, if applicable.

DISCRIMINATORY OR OTHER ILLEGAL CREDIT PRACTICES REVIEW

Examiners did not identify any evidence of discriminatory or other illegal credit practices inconsistent with helping meet community credit needs.

NON-METRO ASSESSMENT AREA – Full-Scope Review

DESCRIPTION OF INSTITUTION’S OPERATIONS IN THE NON-METRO ASSESSMENT AREA

The Non-Metro Assessment Area consists of Clayton and Delaware counties in their entirety, which are non-metropolitan in nature. CSB operates from five offices in the assessment area, which are located in Edgewood, Earlville, Garnavillo, Guttenberg, and Manchester, all in Iowa.

Economic and Demographic Data

According to 2015 ACS Census data, the assessment area consists of 10 census tracts, which includes 9 middle- and 1 upper-income census tracts. The following table illustrates the selected demographic characteristics of the Non-Metro Assessment Area.

|

Demographic Information of the Assessment Area |

|||||||

|

Assessment Area: Non-Metro |

|||||||

|

Demographic Characteristics |

# |

Low % of # |

Moderate % of # |

Middle % of # |

Upper % of # |

NA* % of # |

|

|

Geographies (Census Tracts) |

10 |

0.0 |

0.0 |

90.0 |

10.0 |

0.0 |

|

|

Population by Geography |

35,313 |

0.0 |

0.0 |

91.7 |

8.3 |

0.0 |

|

|

Housing Units by Geography |

17,056 |

0.0 |

0.0 |

92.4 |

7.6 |

0.0 |

|

|

Owner-Occupied Units by Geography |

11,545 |

0.0 |

0.0 |

91.2 |

8.8 |

0.0 |

|

|

Occupied Rental Units by Geography |

3,036 |

0.0 |

0.0 |

93.5 |

6.5 |

0.0 |

|

|

Vacant Units by Geography |

2,475 |

0.0 |

0.0 |

96.2 |

3.8 |

0.0 |

|

|

Businesses by Geography |

3,182 |

0.0 |

0.0 |

91.6 |

8.4 |

0.0 |

|

|

Farms by Geography |

747 |

0.0 |

0.0 |

90.4 |

9.6 |

0.0 |

|

|

Family Distribution by Income Level |

10,018 |

17.9 |

17.1 |

23.4 |

41.5 |

0.0 |

|

|

Household Distribution by Income Level |

14,581 |

20.3 |

16.6 |

19.5 |

43.6 |

0.0 |

|

|

Median Family Income, Non-Metropolitan Statistical Areas (MSAs) - IA |

$61,681 |

Median Housing Value |

$119,229 |

||||

|

|

Median Gross Rent |

$572 |

|||||

|

Families Below Poverty Level |

6.9% |

||||||

|

Source: 2015 ACS; 2020 D&B Data Due to rounding, totals may not equal 100.0% (*) The NA category consists of geographies that have not been assigned an income classification. |

|||||||

According to D&B Data, there are 747 agricultural operations and 3,182 businesses in the assessment area. Service industries represent the largest portion of businesses (by number) at 28.8 percent; followed by agriculture, forestry, and fishing at 19.0 percent; and non-classifiable establishments at 14.0 percent. Additionally, 70.0 percent of businesses in the assessment area have four or fewer employees, and 90.8 percent operate from a single location. The assessment area is

primarily rural in nature and serves to support management’s emphasis on agricultural lending. Management noted that agricultural businesses were not greatly affected by the pandemic, but other businesses (especially those relying on in-person traffic) such as restaurants, small shops, and other businesses in the area were affected by the initial shutdown and subsequent operations under reduced-capacity governmental orders. In addition, businesses were adversely affected by online product sales of competitors, if they did not have an online sales capability. Though the local economy is recovering, residual effects of the pandemic are still being felt in the business community.

The FFIEC estimated median family income levels are used to analyze home mortgage loans under the Borrower Profile criterion and to analyze certain community development activities related to housing. The low-, moderate-, middle, and upper-income categories for non-metropolitan areas of Iowa are detailed in the table below.

|

Median Family Income Ranges |

||||

|

Median Family Incomes |

Low <50% |

Moderate 50% to <80% |

Middle 80% to <120% |

Upper ≥120% |

|

IA Non-Metropolitan Median Family Income |

||||

|

2018 ($67,800) |

<$33,900 |

$33,900 to <$54,240 |

$54,240 to <$81,360 |

≥$81,360 |

|

2019 ($66,900) |

<$33,450 |

$33,450 to <$53,520 |

$53,520 to <$80,280 |

≥$80,280 |

|

2020 ($69,200) |

<$34,600 |

$34,600 to <$55,360 |

$55,360 to <$83,040 |

≥$83,040 |

|

Source: FFIEC |

||||

Competition

The assessment area is moderately competitive regarding the market for financial services. The FDIC Deposit Market Share Report as of June 30, 2020, reported 12 institutions operating from 26 locations within the assessment area. These institutions range in size from small community banks to larger financial institutions with branch locations in the assessment area. CSB ranks second in the assessment area with 12.0 percent market share.

Community Contacts

As part of the evaluation process, examiners contact third parties active in the assessment area to help identify the credit needs and economic conditions of the assessment area. This information helps determine whether local financial institutions are responsive to community credit needs, and provides context regarding available opportunities for area financial institutions. In conjunction with this evaluation, examiners reviewed one existing community contact interview and conducted another with individuals who have specific knowledge of the economic conditions of the assessment area.

The contacts stated that the main economic driver in the assessment area is the agricultural economy, and most of the activity in the assessment area is tied to the agricultural economy in one form or another. The agricultural sector has generally been stable, and the recent pandemic has not greatly affected agricultural producers. Commodity prices are edging higher, but so are the cost of inputs. Consolidation of farming operations continues, though not at the pace it had pre-pandemic. It is hard to enter the farming market, as available land is scarce. Commercial entities were

generally stable with very limited business closures or layoffs in recent years (aside from the effects of the pandemic). Delaware County experienced an expansion of manufacturing activities. Service and retail businesses offer some employment opportunities, as well. Though unemployment was high during the initial months of the pandemic, it has been reduced of late. Some individuals commute to larger cities. The contacts stated that there is a need for more affordable housing units in the assessment area, and that some housing construction has begun in anticipation of announced manufacturing expansions. The contacts also stated that there are no unmet credit needs in the area and financial institutions are willing to provide credit.

Credit and Community Development Needs and Opportunities

Considering information from the community contacts, bank management, and demographic and economic data, examiners determined that small business, small farm, and home mortgage loans are primary credit needs of the assessment area. Call Reports filed by area financial institutions also support this assertion. Further, opportunities for community development exist in the area.

CONCLUSIONS ON PERFORMANCE CRITERIA IN THE NON-METRO ASSESSMENT AREA

LENDING TEST

The institution demonstrated reasonable performance under the Lending Test in the Non-Metro Assessment Area, which is supported by the results of the Borrower Profile criterion.

Geographic Distribution

The Non-Metro Assessment Area does not contain any low- or moderate-income geographies; therefore, examiners did not evaluate the geographic distribution of loans, as a review would not have resulted in meaningful conclusions.

Borrower Profile

The distribution of borrowers reflects reasonable penetration among farms and businesses of different revenue sizes and individuals of different income levels. The institution’s reasonable performance in each loan category supports this conclusion.

Small Farm Lending

The distribution of borrowers reflects reasonable penetration among farms of different revenue sizes. The initial review showed that the institution’s level of lending is substantially below that of D&B benchmark data; however, further review showed an anomaly in the random sample. Specifically, of the 16 loans to farm with gross annual revenues of over $1 million, 14 of them were made to two entities, thus inflating the percentage in that category. Management indicated that one of the customers had five loans and was originally smaller than $1 million gross annual revenues at the beginning of the banking relationship and grew larger over time. The borrower with nine of the loans is a cattle operation, which typically have higher revenue streams than other agricultural operations in the area.